Featured

Table of Contents

Trustees can be household members, relied on people, or financial organizations, depending on your preferences and the intricacy of the trust. The objective is to ensure that the count on is well-funded to satisfy the child's lasting monetary requirements.

The duty of a in a youngster assistance trust fund can not be underrated. The trustee is the specific or organization liable for taking care of the trust fund's properties and ensuring that funds are dispersed according to the terms of the trust fund agreement. This includes making certain that funds are used solely for the kid's advantage whether that's for education and learning, clinical care, or everyday expenses.

They have to likewise provide regular records to the court, the custodial parent, or both, relying on the terms of the count on. This accountability guarantees that the trust fund is being managed in a manner that benefits the youngster, avoiding abuse of the funds. The trustee additionally has a fiduciary task, meaning they are legitimately obligated to act in the most effective interest of the kid.

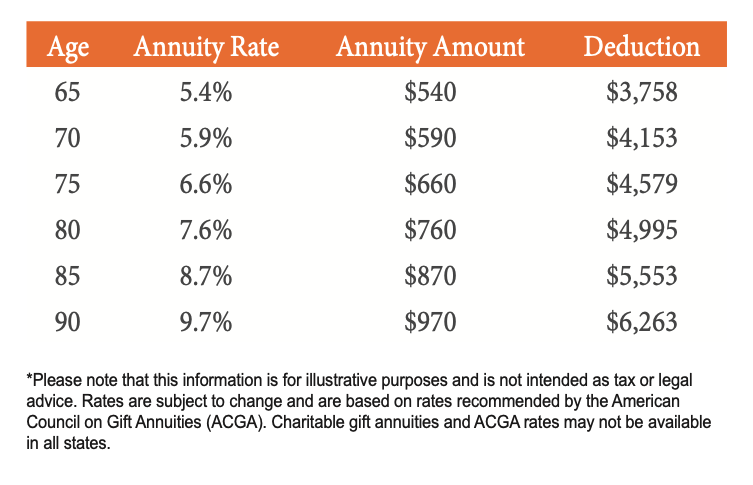

By purchasing an annuity, moms and dads can guarantee that a dealt with quantity is paid out consistently, regardless of any kind of variations in their earnings. This gives tranquility of mind, recognizing that the kid's needs will certainly remain to be satisfied, regardless of the monetary scenarios. One of the crucial advantages of using annuities for child support is that they can bypass the probate procedure.

What should I look for in an Immediate Annuities plan?

Annuities can additionally offer protection from market variations, guaranteeing that the child's financial backing continues to be steady also in unpredictable financial problems. Annuities for Kid Assistance: A Structured Option When establishing, it's necessary to take into consideration the tax effects for both the paying parent and the youngster. Trusts, depending upon their framework, can have different tax obligation therapies.

In various other cases, the beneficiary the kid might be accountable for paying tax obligations on any type of distributions they obtain. can additionally have tax effects. While annuities supply a secure earnings stream, it is essential to understand just how that income will certainly be taxed. Depending on the structure of the annuity, settlements to the custodial moms and dad or child might be taken into consideration taxable earnings.

One of the most considerable advantages of utilizing is the capability to safeguard a youngster's financial future. Counts on, particularly, use a level of security from financial institutions and can ensure that funds are used responsibly. As an example, a trust can be structured to ensure that funds are only used for certain objectives, such as education and learning or health care, protecting against abuse - Tax-efficient annuities.

Annuities

No, a Texas kid support count on is particularly made to cover the kid's important needs, such as education, medical care, and day-to-day living costs. The trustee is lawfully obliged to guarantee that the funds are used exclusively for the advantage of the youngster as described in the trust fund contract. An annuity gives structured, predictable payments in time, making certain constant monetary support for the kid.

Yes, both child assistance trust funds and annuities included prospective tax obligation effects. Trust fund income may be taxable, and annuity repayments might likewise go through tax obligations, depending upon their framework. It is essential to seek advice from a tax specialist or economic consultant to understand the tax duties connected with these financial tools.

How do Long-term Care Annuities provide guaranteed income?

Download this PDF - Sight all Publications The elderly person populace is huge, growing, and by some quotes, hold two-thirds of the specific riches in the United States. By the year 2050, the variety of elders is forecasted to be nearly two times as big as it was in 2012. Because numerous senior citizens have been able to conserve up a nest egg for their retirement years, they are often targeted with scams in such a way that younger individuals without any savings are not.

In this atmosphere, customers need to arm themselves with info to shield their passions. The Lawyer General gives the complying with ideas to consider before purchasing an annuity: Annuities are challenging financial investments. Some bear facility high qualities of both insurance and safety and securities products. Annuities can be structured as variable annuities, fixed annuities, immediate annuities, deferred annuities, and so on.

Consumers need to read and understand the syllabus, and the volatility of each financial investment noted in the prospectus. Financiers need to ask their broker to clarify all terms and conditions in the prospectus, and ask questions concerning anything they do not recognize. Repaired annuity products may additionally bring threats, such as long-term deferment periods, disallowing financiers from accessing every one of their cash.

The Lawyer General has submitted lawsuits against insurance provider that sold improper postponed annuities with over 15 year deferral periods to investors not anticipated to live that long, or that require access to their money for wellness treatment or assisted living expenditures (Guaranteed return annuities). Investors must see to it they understand the lasting consequences of any kind of annuity purchase

What is the best way to compare Guaranteed Income Annuities plans?

Beware of workshops that provide free dishes or gifts. In the end, they are rarely complimentary. Be cautious of representatives that offer themselves fake titles to improve their reliability. One of the most considerable charge connected with annuities is commonly the abandonment charge. This is the percentage that a consumer is billed if she or he takes out funds early.

Customers might wish to consult a tax obligation specialist before buying an annuity. The "safety" of the investment depends on the annuity. Be cautious of representatives who aggressively market annuities as being as safe as or much better than CDs. The SEC warns consumers that some vendors of annuities items prompt customers to switch to an additional annuity, a technique called "churning." Regrettably, representatives may not adequately disclose costs associated with switching investments, such as brand-new abandonment charges (which typically begin over from the date the item is switched), or dramatically transformed benefits.

Representatives and insurer may provide incentives to entice investors, such as additional rate of interest factors on their return. The advantages of such "benefits" are typically outweighed by increased costs and management costs to the capitalist. "Bonuses" may be just marketing gimmicks. Some deceitful representatives encourage customers to make impractical investments they can't pay for, or purchase a lasting deferred annuity, although they will certainly require accessibility to their cash for healthcare or living costs.

This area gives information beneficial to retirees and their families. There are lots of events that could influence your benefits. Provides information frequently asked for by brand-new retirees including transforming wellness and life insurance coverage alternatives, Sodas, annuity settlements, and taxable sections of annuity. Explains just how advantages are influenced by occasions such as marriage, divorce, death of a partner, re-employment in Federal service, or failure to take care of one's funds.

How do I apply for an Lifetime Payout Annuities?

Trick Takeaways The beneficiary of an annuity is an individual or company the annuity's proprietor designates to receive the agreement's survivor benefit. Various annuities pay out to recipients in various ways. Some annuities might pay the beneficiary stable repayments after the agreement owner's death, while other annuities may pay a fatality advantage as a swelling amount.

{kind=link}

Table of Contents

Latest Posts

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Variable Annuities Vs Fixed Annuiti

Understanding Financial Strategies Everything You Need to Know About Financial Strategies What Is Annuities Fixed Vs Variable? Benefits of Choosing the Right Financial Plan Why Variable Annuities Vs F

Breaking Down Your Investment Choices A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Advantages and Disadvantages of Different Retirement Plans Why Fixed Indexed An

More

Latest Posts